The UK property market remains one of the most stable and attractive destinations for international capital, but the legal landscape in 2026 is far from simple. Whilst there are no restrictions on your right to buy, the reality of uk property law for foreign nationals now involves a complex web of residency tests and stringent transparency requirements. You likely recognise the prestige of a UK postcode, yet the fear of a surprise Stamp Duty bill or the anxiety of a rigorous compliance check can be daunting. It is a common concern, especially when the line between ‘resident’ and ‘tax resident’ feels increasingly blurred.

This guide offers the expert legal clarity you need to manage these complexities without the fear of unexpected tax liabilities. We’ll provide a definitive roadmap of the 2026 purchase process, from the mandatory registration of overseas entities with Companies House to the latest 60-day reporting deadlines for Capital Gains Tax. By understanding how to legally minimise your tax exposure and finding a solicitor who values discreet, high-standard service, you can secure your British assets with absolute peace of mind.

Key Takeaways

- Confirm your legal right to own British real estate and understand the strategic differences between purchasing for personal use and commercial development.

- Navigate the financial complexities of uk property law for foreign nationals, including the specific criteria for reclaiming the 2% non-resident Stamp Duty surcharge.

- Streamline your purchase through remote conveyancing protocols that facilitate secure identity verification and document completion from anywhere in the world.

- Determine the most tax-efficient ownership structure by weighing the benefits of personal title against the administrative requirements of registering an overseas entity.

- Protect your long-term investment by mastering the unique British concepts of leasehold and freehold to mitigate the risks of rising ground rents.

Can Foreign Nationals Buy Property in the UK? 2026 Legal Framework

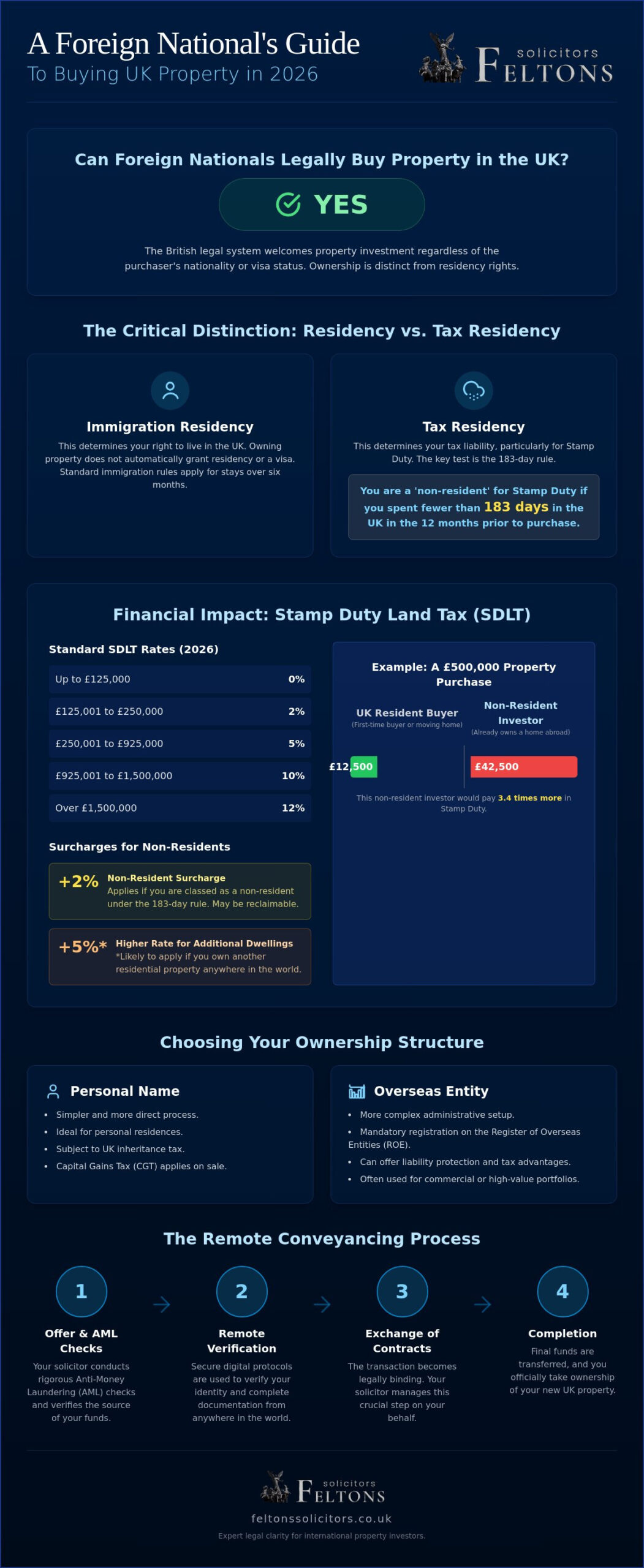

The UK remains one of the world’s most accessible property markets. Unlike many other nations that impose strict quotas or outright bans on international buyers, the British legal system welcomes investment regardless of the purchaser’s nationality. Understanding uk property law for foreign nationals is the first step toward a successful acquisition. You don’t need a UK passport or even a visa to own a piece of British soil; the market is open for personal residences, buy-to-let portfolios, and large-scale commercial developments alike.

This openness is underpinned by the stability of English land law, which provides a level of certainty and protection that few other jurisdictions can match. Even with the introduction of stricter transparency measures like the Register of Overseas Entities (ROE), the UK is still viewed as a ‘safe haven’ for international wealth. These regulations are designed to bolster market integrity rather than deter genuine investors. However, it’s vital to separate the right to own property from the right to live in it. Owning a house in London or a cottage in the Cotswolds doesn’t grant you residency rights or a path to a UK visa. You’ll still need to comply with standard immigration rules for stays exceeding six months.

Residency vs. Tax Residency: The 183-Day Rule

In 2026, the distinction between your immigration status and your tax residency is sharper than ever. For property transactions, the UK government uses a specific ‘non-resident’ test. You’re generally classed as a non-resident for Stamp Duty purposes if you’ve spent fewer than 183 days in the UK during the 12 months before your purchase. This isn’t just a technicality; it’s the trigger for a 2% surcharge on your Stamp Duty Land Tax (SDLT) bill. This rule applies even if you’re a British citizen living abroad or have a valid work visa.

The Role of the Solicitor in International Transactions

Managing a cross-border purchase requires more than just standard legal work. It demands a solicitor who understands the nuances of international wealth structures and the rigour of modern Anti-Money Laundering (AML) checks. Feltons Solicitors acts as a calm, steady guide during this process, ensuring all documentation is handled with discreet precision. We manage the ‘Exchange of Contracts’ and identity verification remotely, allowing you to secure your investment without needing to be physically present in the UK. Our role is to provide a boutique level of care, ensuring your transaction moves from offer to completion with absolute legal clarity whilst protecting your privacy at every stage.

The Financial Impact: SDLT Surcharges and Tax Residency Rules

Financial planning for a UK acquisition requires a granular understanding of the current tax regime. Whilst the market is open, the costs of entry are tiered based on your residency status and your existing global property portfolio. A fundamental pillar of uk property law for foreign nationals is the Stamp Duty Land Tax (SDLT), which is a graduated tax payable on the purchase price of a property. For residential purchases in England and Northern Ireland, the standard rates for 2026 follow a clear structure:

- Up to £125,000: 0%

- £125,001 to £250,000: 2%

- £250,001 to £925,000: 5%

- £925,001 to £1,500,000: 10%

- Over £1,500,000: 12%

Foreign buyers must account for significant surcharges that sit atop these figures. A 2% surcharge applies to any non-UK resident purchasing a residential property costing £40,000 or more. If you already own a residential property anywhere else in the world, an additional 5% surcharge is likely to apply. This means an international investor could face a top-slice SDLT rate of 19% on the portion of the price above £1.5 million. Detailed guidance on Stamp Duty Land Tax for non-UK residents confirms that the 2% surcharge can sometimes be reclaimed if you spend more than 183 days in the UK during the year following your purchase.

Calculating Your Total Tax Liability

The total cost of your investment isn’t just the purchase price. A UK resident buying a £500,000 home might pay £12,500 in SDLT; however, a non-resident investor buying that same property as a second home could pay up to £47,500. It’s a stark difference that demands early budgeting. If a property is purchased jointly by a resident and a non-resident, the 2% surcharge is typically applied to the entire transaction value. You might find relief if the property is classed as commercial or mixed-use, as these transactions usually avoid the non-resident surcharge entirely. Engaging a firm with expertise in residential conveyancing ensures these calculations are precise from the outset.

Ongoing Tax Obligations for Foreign Landlords

Owning the asset is only the first stage of your tax journey. If you let the property, you’re subject to the Non-Resident Landlord Scheme (NRLS), where tenants or agents must withhold 20% of the rent for HMRC unless you’ve been authorised to receive gross payments. When you eventually decide to sell, you’ll need to navigate Capital Gains Tax (CGT), currently set at 18% for basic rate taxpayers and 24% for higher earners. You must report the sale and settle any CGT due within 60 days of completion, regardless of whether a tax liability actually exists. This rigorous reporting cycle reflects the UK’s commitment to transparency in uk property law for foreign nationals.

Navigating the Legal Conveyancing Process and Compliance Requirements

The journey from making an initial offer to receiving the keys is a structured legal process that demands meticulous attention to detail. In the context of uk property law for foreign nationals, this journey typically spans eight to twelve weeks, though complex international chains can extend this timeline. Once your offer is accepted, your solicitor begins the ‘Enquiries’ phase, scrutinising the title deeds and local authority searches to ensure no hidden liabilities exist. Whilst this happens, you should commission a comprehensive structural survey. Many British properties, particularly in historic urban centres, are sold as leaseholds. A survey is vital to identify potential maintenance issues or structural defects that could lead to significant future costs.

Remote conveyancing has become the standard for international clients. Modern legal practices use secure digital platforms for identity verification and document signing, meaning you rarely need to visit the UK in person to finalise your purchase. The most critical milestone is the ‘Exchange of Contracts’. At this point, the agreement becomes legally binding. In UK law, this is the point of no return; if you withdraw after this stage, you will likely lose your deposit and may face litigation for breach of contract. Completion follows shortly after, which is when the balance of funds is transferred and ownership officially passes to you.

Anti-Money Laundering (AML) and Source of Funds

Compliance is the most significant hurdle for many overseas buyers. UK law requires solicitors to perform exhaustive ‘Know Your Customer’ (KYC) checks to prevent financial crime. You’ll need to provide clear documentation regarding your ‘Source of Wealth’, which explains how you accumulated your total assets, and your ‘Source of Funds’ for this specific purchase. Common pitfalls include using offshore accounts without a clear audit trail or receiving gifted deposits from relatives without proper legal declarations. Providing this information early prevents delays and ensures you meet the Stamp Duty Land Tax rules for non-UK residents without administrative friction.

Securing Financing: UK Mortgages for Overseas Buyers

Securing a UK mortgage as a foreign national is entirely possible, though the criteria are stricter than for residents. Most lenders require a higher deposit, typically between 20% and 40% of the property value. Interest rates for ‘Expat’ or non-resident loans are generally higher, reflecting the lender’s perceived risk. You’ll also need to establish a UK-based bank account for monthly repayments. Navigating uk property law for foreign nationals effectively means having these financial arrangements in place before you begin your property search to demonstrate your status as a serious buyer.

Ownership Structures: Personal Names vs. Registering Overseas Entities

Deciding how to hold your British assets is a choice that balances administrative simplicity against long-term tax efficiency. Buying in a personal name is the most straightforward path. It avoids the complexities of company filings and the necessity for annual accounts. However, many sophisticated investors prefer using a UK Limited Company, particularly when building a portfolio. This structure can offer significant advantages regarding mortgage interest relief and Corporation Tax rates, though it does come with higher ongoing administrative costs. This choice is a central pillar of uk property law for foreign nationals and should be made after considering your exit strategy and global tax position.

If you choose to buy through a foreign company, you must comply with the Register of Overseas Entities (ROE). This requirement, introduced under the Economic Crime (Transparency and Enforcement) Act 2022, is mandatory for any foreign entity that wants to buy, sell, or lease land in the UK. The process involves a £250 digital registration fee and an annual update statement that costs £134. Feltons Solicitors provides a bespoke service for overseas entity beneficial owner registration, ensuring your investment remains fully compliant and marketable whilst protecting your privacy where legally permitted.

The Register of Overseas Entities (ROE) Explained

Transparency is the driving force behind the ROE. Foreign companies holding UK land must declare their beneficial owners and managing officers to Companies House. A UK-regulated agent must verify this information before the entity can be registered. The consequences of non-compliance are severe. Without a valid Overseas Entity ID, you’ll be unable to register your title at the Land Registry, effectively preventing you from selling, leasing, or charging the property. Failure to update the register annually is also a criminal offence, which can lead to daily fines or even imprisonment for company officers.

Joint Ownership Options: Tenants in Common vs. Joint Tenants

For those buying with a partner or business associate, the legal structure of that partnership is vital. Joint Tenants own the property together as a single legal entity; if one owner passes away, their share automatically transfers to the survivor. Conversely, Tenants in Common own specific, defined shares, which can be passed on via a Will to anyone of their choosing. This is often the preferred route for international wealth protection, as it allows for more flexible estate planning. We strongly recommend a ‘Declaration of Trust’ to clearly define these shares and protect each party’s interests. Professional support for the Registration of Overseas Entities ensures your ownership structure is robust from the outset.

Managing Your Investment: Leasehold Rights and Estate Planning

Securing your property is only the beginning of your journey with uk property law for foreign nationals. In England and Wales, a significant portion of urban property, particularly apartments, is sold as leasehold. This means you own the right to occupy the building for a set period, whilst the ‘freeholder’ retains ownership of the land itself. It’s a unique legal concept that requires active management. You must stay vigilant regarding ground rents and service charges; if these costs rise disproportionately, they can diminish the marketability and value of your asset. Professional leasehold management ensures your rights are protected and your investment remains a stable pillar of your international portfolio.

You must also look ahead to the eventual transfer of your wealth. UK-sited assets, including all residential property, are generally subject to UK Inheritance Tax (IHT). Currently, this is charged at a rate of 40% on any value exceeding the £325,000 nil-rate band. Whilst an additional residence nil-rate band of up to £175,000 may be available if you leave a home to direct descendants, the criteria are strict. It’s also vital to note that from April 2025, the UK moved to a residency-based system for IHT. Individuals who’ve been UK residents for 10 of the previous 20 tax years may find their worldwide assets fall within the UK tax net. Relying on a foreign Will to dispose of a British home often leads to significant delays and legal friction. A dedicated UK Will ensures your property is handled according to English law with minimal administrative burden.

Lease Extensions and Enfranchisement for Overseas Owners

For those owning flats, the statutory right to extend your lease becomes available after two years of continuous ownership. This is a vital mechanism for preserving the value of your asset. Leases with fewer than 80 years remaining can become significantly more expensive to extend and difficult to remortgage. Our leasehold enfranchisement experts provide pragmatic advice on navigating these claims. We manage the entire process, including complex negotiations and dispute resolution with freeholders, ensuring your interests are represented whilst you are abroad.

Succession and Estate Planning for International Clients

UK property doesn’t exist in a vacuum; it sits within the context of your global estate. This creates a potential risk of double taxation depending on the treaties between the UK and your home jurisdiction. Integrating your British assets into a comprehensive estate planning strategy allows for the legal minimisation of tax exposure. Managing these matters requires a specialist firm that understands the nuances of international wealth structures. We act as a discreet partner, ensuring your legacy is protected and that your beneficiaries aren’t left navigating a complex legal maze without expert guidance.

Securing Your British Assets with Confidence

The UK property market remains a premier destination for global investors, yet the path to a successful acquisition in 2026 is paved with specific regulatory obligations. We’ve explored how understanding the nuances of uk property law for foreign nationals is essential, from managing the 2% non-resident Stamp Duty surcharge to ensuring your company is correctly listed on the Register of Overseas Entities. Success isn’t just about the initial purchase; it requires a proactive approach to leasehold management and robust estate planning to protect your legacy against future tax liabilities.

At Feltons Solicitors, we act as your discreet partner throughout this journey. We provide pragmatic, expert advice for international clients, specialising in the Registration of Overseas Entities and comprehensive property services. Whether you’re navigating the complexities of cross-border wealth structures or securing your assets for the next generation, our team offers the steady guidance you deserve. Contact Feltons Solicitors for expert guidance on your UK property purchase and ensure your investment is built on a foundation of absolute legal clarity. Your British property journey should be a source of security, not stress.

Frequently Asked Questions

Do I need to be in the UK to complete a property purchase?

You don’t need to be physically present in the UK to finalise your transaction. Remote conveyancing allows solicitors to manage identity verification and the exchange of contracts through secure digital platforms. Whilst you’ll need to provide certified documents, the entire process from offer to completion can be handled from your home country with ease.

Can I buy property in the UK if I have a criminal record in my home country?

Generally, yes, as there are no legal restrictions preventing those with a criminal record from owning British real estate. However, you’ll face much more rigorous Anti-Money Laundering checks during the purchase process. Mortgage lenders may also view your application with increased scrutiny, so it’s vital to be transparent with your legal team from the outset.

How much is the non-resident Stamp Duty surcharge in 2026?

The non-resident surcharge remains at 2% for the 2026 tax year. This is a flat rate added to the standard Stamp Duty Land Tax (SDLT) brackets for residential properties costing £40,000 or more. It’s a critical component of uk property law for foreign nationals that applies if you haven’t been present in the UK for at least 183 days in the 12 months prior to your purchase.

Is it better to buy UK property in a company name or personal name?

The right choice depends on your long-term investment strategy and your total portfolio size. Purchasing in a personal name is simpler and avoids the costs associated with the Register of Overseas Entities. Conversely, using a UK Limited Company can be more tax-efficient for buy-to-let investors, though it involves higher administrative fees and mandatory annual filings. Navigating uk property law for foreign nationals requires weighing these administrative burdens against potential tax savings.

What documents do I need to prove my source of funds as a foreign national?

You’ll need to provide a clear audit trail showing exactly how your capital was acquired. This typically includes six months of bank statements, payslips, or tax returns from your home country. If your funds come from the sale of an asset or an inheritance, you’ll need the corresponding legal documentation to satisfy the UK’s strict ‘Know Your Customer’ requirements.

Can I get a UK mortgage if I don’t have a UK credit history?

You can secure a mortgage without a UK credit history by using specialist international or ‘Expat’ lenders. These providers assess your global wealth and income rather than just your UK credit file. You should expect to provide a larger deposit, often between 25% and 40% of the property value, and pay slightly higher interest rates than a UK resident.

Does buying a house in London or the UK give me a ‘Golden Visa’?

No, property ownership does not grant any residency or immigration rights in the UK. The British government doesn’t offer a ‘Golden Visa’ or investment-based residency through real estate purchases. You must still meet standard visa requirements if you intend to live in the property for more than six months a year, regardless of the property’s value.

What happens to my UK property if I die without a UK Will?

Your British assets will be distributed according to the UK’s intestacy rules, which may not align with your personal wishes or your home country’s laws. This process is often slow and expensive for international families, potentially leading to significant Inheritance Tax complications. Drafting a specific UK Will is the only way to ensure your property passes to your chosen beneficiaries without unnecessary legal friction.